Discover more about S&P Global’s offerings

Combining 451 Research’s industry-leading analysis with a proprietary global panel of IT decision-makers, Voice of the Enterprise: Digital Pulse tracks the disruption occurring in the market and exposes the major impacts and opportunities for enterprises, IT vendors, suppliers and investors. This survey was designed to measure the impact of the COVID-19 coronavirus outbreak on businesses. It was conducted between May 26 and June 11, 2020, and represents approximately 575 completes from pre-qualified IT decision-makers.

By: Liam Eagle, Research VP and GM, Voice of the Enterprise and Voice of the Service Provider

Published: June 1, 2020

Fewer businesses have faced major disruption than expected to. Some 13% of organizations say they have experienced a major disruption (e.g., loss of a major client, inability to meet debt obligations). In March, 8% had already experienced such a disruption and another 39% felt they would within three months. In our June survey, 41% of organizations feel they could go indefinitely without such a disruption, compared to 28% who felt that way in March.

A new WFH standard is here to stay for most companies. Two-thirds of organizations (67%) expect expanded or universal WFH policies implemented in response to the outbreak will remain in place long-term or permanently, a significant increase from the 38% that expressed this expectation in March.

Organizations are preparing for a long period of altered working conditions. Many businesses expect to spend more on employee communication and collaboration (43%), mobile devices and services (37%), bandwidth and network capacity (32%), and information security (28%) among other things.

Almost half of companies expect to reduce office space. Nearly half (47%) of organizations with office space say they expect to reduce their physical office footprint as a result of the coronavirus outbreak. More than 20% expect to reduce it by more than 25%.

Many businesses are seeking flexible terms from suppliers. Just over half (56%) of organizations agree they are offering to adjust the terms of leases, licenses or contracts for their customers. However, only 42% of organizations say they are expecting or asking IT vendors to adjust payment pricing, payment terms or payment models.

Read more Covid-19 Impact content from 451 Research >

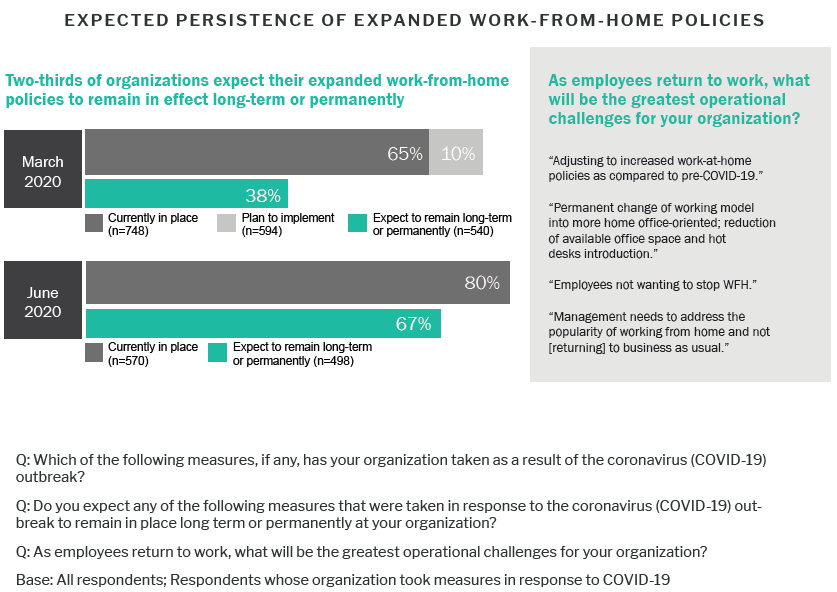

Among policy responses to the coronavirus outbreak, expanded or universal WFH policies were implemented broadly and quickly by a large majority of organizations. By the time our June Flash Survey fielded, most organizations expected those expanded WFH policies to remain in place long-term or permanently.

Rapid and near-universal implementation. Even in early March, 65% of organizations had these policies in place, and another 10% expected to implement. In June, 80% of organizations say they have expanded WFH policies in place. Rare exceptions include the smallest companies, with fewer than 250 employees (68% implemented) or those with less than $1m in annual revenue (45%), possibly due to a greater likelihood of already having non-standard working environments (e.g., fully remote staff).

A new standard of working. Twothirds of organizations (67%) expect expanded WFH policies to remain in place, a significant increase from the 38% that expressed this expectation in March. This too is higher among the largest companies and lower among the smallest. Companies identified as digital transformation laggards are also less likely to expect to retain new WFH policies.

The outbreak has been a proof-ofconcept for working from home. The sharp increase in plans for longerterm adoption is likely due to the effectiveness of remote working systems these companies have implemented, and the desire for a return on investments they have made in enabling it.

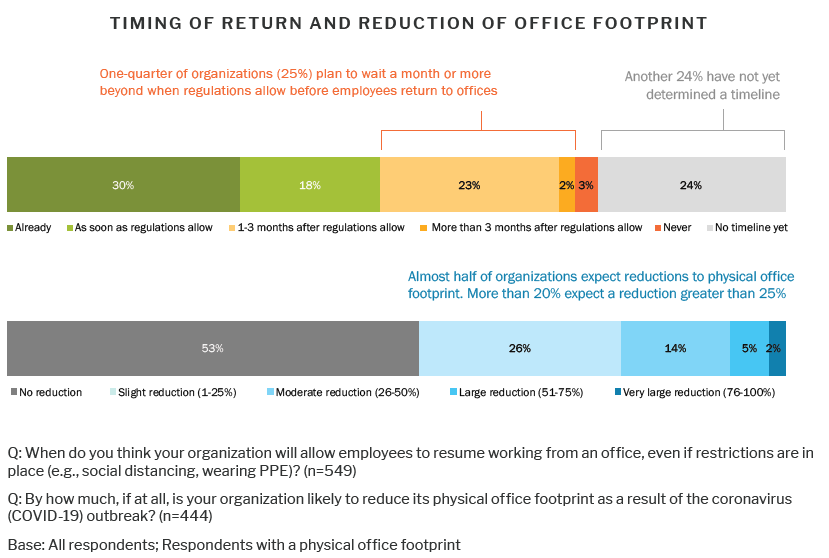

The relative success of WFH efforts and the difficulties presented by the prospect of returning to work in physical office environments (in particular, the conflict between close proximity and employee safety) have many companies expressing plans to delay their return, and a significant portion expecting to reduce their office footprint.

Caution around returning to workplaces is common. Although 18% of organizations intend to have employees return to working from offices as soon as local regulations allow, 25% will wait a month or more. Another 24% have not yet determined a timeline. Unsurprisingly, publicsector firms are the most likely (31%) to follow regulatory guidance to the letter. Among companies fewer than 10 years old, 10% say employees would never return to an office.

Almost half of companies expect to reduce office space. Forty-seven percent of organizations with office space say they expect to reduce their physical office footprint as a result of the coronavirus outbreak. More than 20% expect to reduce it by more than 25%. Across all vertical categories, only finance and software and IT services see more than half of companies expecting some reduction (53% and 51%, respectively). Office reductions are most common at the largest firms – 60% of companies with more than $10bn in revenue expect to reduce office footprint.

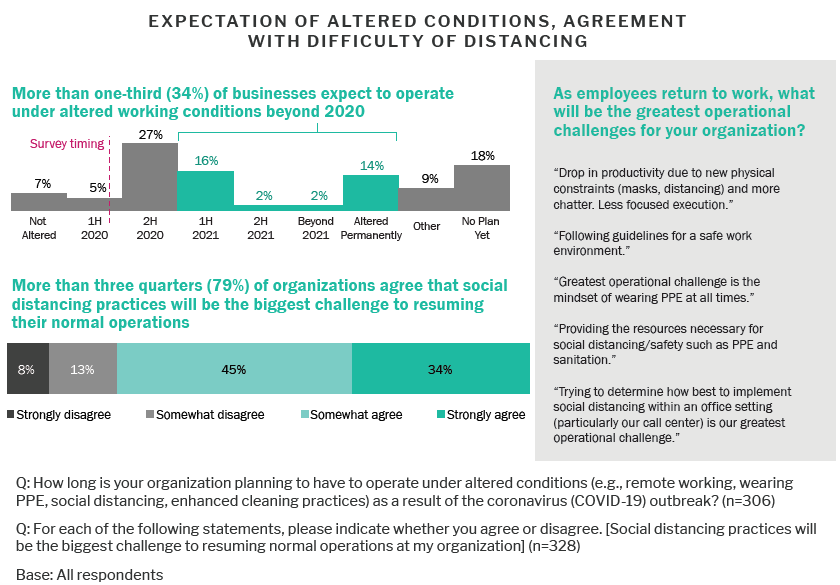

Although a notable segment of organizations is optimistically planning for altered working conditions (such as social distancing, wearing PPE and enhanced cleaning practices) to end this calendar year, caution and uncertainty are also common attitudes around returning to the workplace.

Enterprises are preparing for a long period of altered working conditions. More than a third (34%) of organizations are expecting altered conditions to remain in place until 2021 or beyond. Fourteen percent say conditions have been altered permanently. Uncertainty is also a factor, with 18% of organizations indicating they don’t yet have an expectation for when altered conditions will end.

Distancing will be the greatest barrier to returning. A significant majority (79%) of organizations agree that social distancing practices will be the biggest challenge to resuming their normal operations. Agreement is especially strong in the financial services sector (93%). There is no grouping of companies that stands out as mostly disagreeing.

In response to an open-ended question about the greatest operational challenges surrounding the return to work, companies repeatedly cite social distancing and employee health and safety as critical challenges.

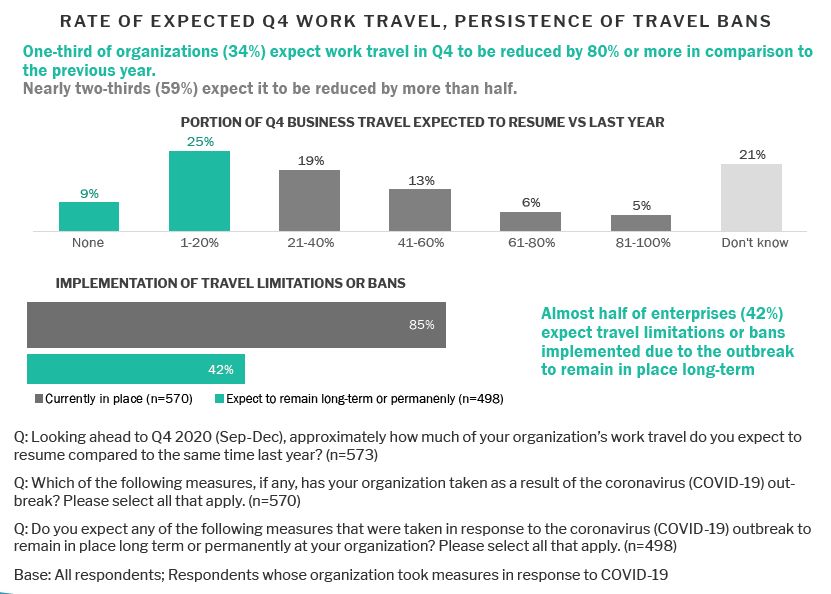

Business travel has been almost universally on hold throughout the outbreak, both as an act of caution by businesses and imposed by government regulations restricting travel. However, even as organizations plan their return to regular office environments, they remain cautious regarding travel plans.

Many organizations expect a small, incremental return to travel in Q4. A third of organizations (34%) expect work travel in Q4 to be reduced by 80% or more in comparison to the previous year, while 59% expect it to be reduced by more than half.

Uncertainty remains – 21% of organizations say they don’t yet know the extent to which work travel will return in Q4. This uncertainty is particularly strong in the retail (35%) and manufacturing (28%) sectors.

Limitations are likely to remain in place. Forty-two percent of organizations expect travel limitations or bans put in place because of the outbreak to remain long-term, a significant increase from March, when 22% of organizations expressed the same expectation. Enterprises are finding ways to operate in the absence of travel, are averse to undue risk, may see a potential avenue for cost savings in a financially challenging period and are likely to apply a greater level of scrutiny to future business travel.

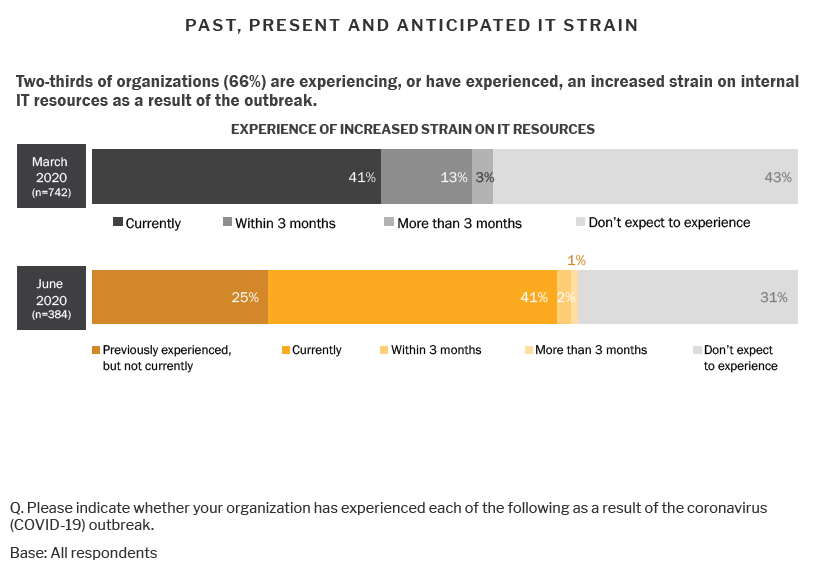

Survey responses suggest the demands of dealing with the coronavirus outbreak are placing a strain on enterprise IT resources. The portion of businesses indicating they were currently or had previously experienced such a strain as an outcome of the coronavirus outbreak increased substantially between March and June 2020.

IT resource strain has been more widespread than anticipated. Forty-one percent of organizations surveyed in June 2020 say they’re experiencing an increased strain on internal IT resources as a result of the outbreak. Another 25% say they have experienced increased IT strain but are not currently. This impact reaching more than two-thirds of organizations is broader than was expected in March, when 43% said they didn’t expect to experience an increased IT strain.

Enterprises are successfully addressing this strain. A quarter (25%) of organizations indicate they have experienced, but are no longer experiencing, increased IT resource strain. This is the largest recovery among the types of impact measured, and it suggests they have, among other things, cleared the hurdle of enabling broader WFH practices. Only 3% of organizations expect to experience such strain in the future, suggesting that enterprises feel they are trending toward recovery.

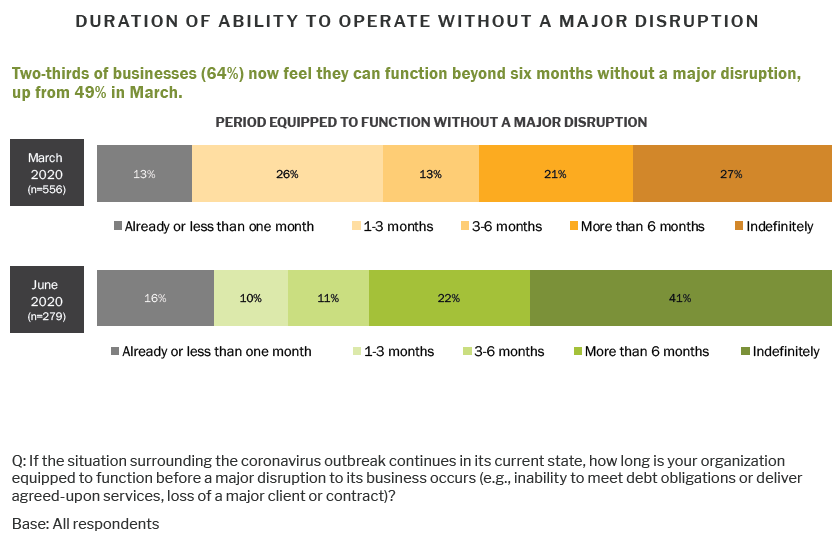

Enterprises responding to the March survey painted a troubling picture of the prospect for major disruption (meaning inability to meet debt obligations or deliver an agreed-upon service, or the loss of a major client). Months later, their fears have mostly not materialized, and businesses are expressing more optimism about their resilience in the face of the outbreak.

Major disruption has mostly not materialized. In March, 8% of organizations had already experienced such a disruption with 5% expecting it within a month, and another 26% expecting it within three months. Three months later, that disruption has mostly failed to materialize. Currently, 13% of organizations say they have experienced a major disruption, an increase of only five percentage points versus March.

Increasing optimism around longevity. In our June survey, 63% feel they could go longer than six months without a major disruption (including 41% that feel equipped to carry on indefinitely), given continuing outbreak circumstances. This was up from 48% in March.

Businesses may have avoided disruption due to increased efficiency, other operational shifts, government-initiated stimulus or some combination of these and other factors.

When we conducted our March flash survey, organizations were in the process of establishing WFH policies and implementing the technology and practices that would support this mode of working. Although many of them were struggling with productivity at the time, that struggle has lessened in the months since, and a portion of those affected has seen productivity recover.

Productivity prospects are improving. While 28% of organizations say they are experiencing a reduction in employee productivity as a result of the outbreak, 12% have experienced it, but are not currently. Combined, this almost exactly accounts for the 40% that said they were experiencing productivity loss in March. That position of lost-andrecovered productivity is most prominent in the finance (36%) and communications, media and publishing (35%) verticals.

Little future impact expected. The 22% of organizations that previously expected a productivity impact within three months has not seen it materialize to the extent expected. Just 3% of organizations now expect a reduction in productivity, in or beyond the next three months, with 57% saying they do not expect to experience it.

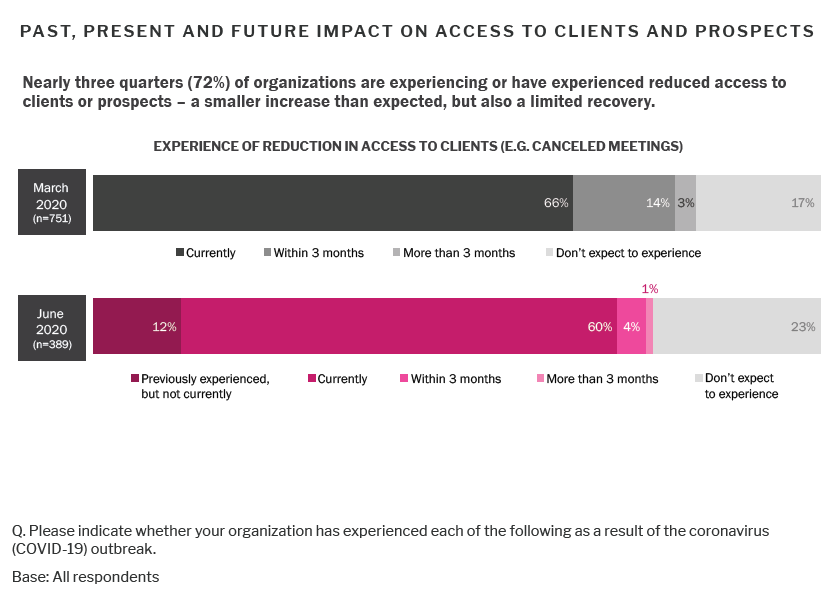

Reduced access to clients and prospects continues to be among the most broadly felt of the outbreak’s impacts on businesses, from canceled meetings to gaps in typical sales processes and greater customer caution around spending. Enterprises continue to widely report limits to access.

Limited access has not improved for many. Sixty percent of organizations are facing reduced access to clients or prospects as a result of the outbreak, with another 12% saying they have experienced it, but are not currently. This impact is smaller than was expected in March, when 66% were experiencing reduced access and 14% expected to within three months.

A saturation point. Although relatively few organizations have seen the issue of reduced access improve, only a few (5%) expect to begin experiencing it. Nearly a quarter (23%) say they do not expect to.

While we have seen workforce productivity effectively addressed with collaboration tools, the shift to a digital customer experience is a larger, more transformational effort. We may continue to see companies struggling to solve the new business pipeline issue, and its resulting impacts on financial performance.

Most organizations indicate spending is unchanged by the coronavirus outbreak in each case. However, in many categories, close to half of respondents indicate an outbreak motivated spending change, with some such as IT resources and information security leaning distinctly toward spending increases.

A growing cost to operating, securing IT. Companies that indicate spending increases outnumber those spending less most significantly in the categories of IT resources and assets (31% to 18%) and information security (28% to 7%). Compared to March, security spending increases grew more common (from 15% to 28%), while IT resources and assets saw an increased proportion of decreases (from 3% to 18%) while remaining weighted toward increase.

Specifically, organizations are spending more on communication and collaboration technologies (50%), employee devices and services (43%), information security tools (42%) and network capacity (38%).

Incremental growth in technology product spending. For almost every category of technology product and service, a greater portion of organizations have increased spending in June than had in March. These are mostly small increases, except for the information security sector, which jumps 14 percentage points.

Information security is a critical facet of our coronavirus coverage, and of this flash survey. More detailed views of the survey’s security outcomes will follow via our Information Security channel coverage

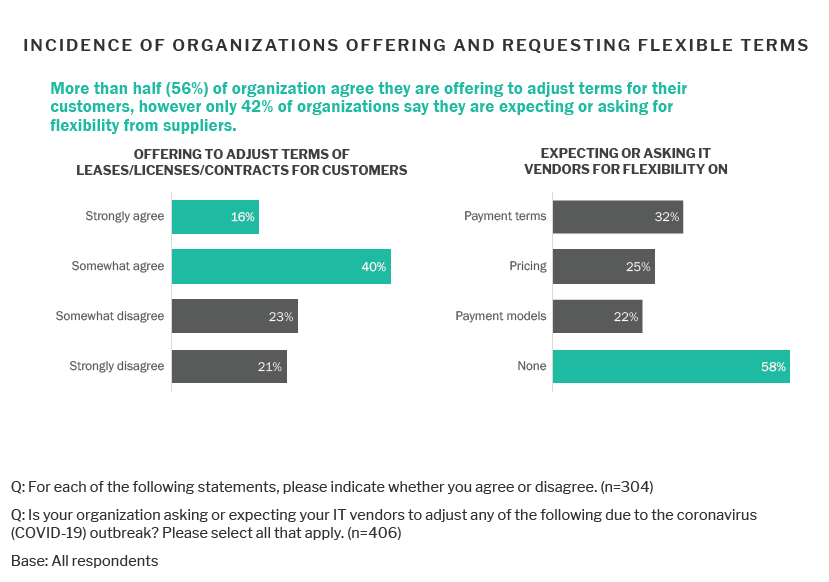

With impacts on access to customers, levels of demand and – in some cases – the continued existence of those customers, the coronavirus outbreak has created issues of cash flow and liquidity for organizations of many sizes and types. In many cases, this has led to both the desire for, and the establishment of, new flexibility in pricing, terms and payment models.

Enterprises are making their offerings more flexible. More than half of organizations (56%) agree they are offering to adjust the terms of leases, licenses or contracts for their customers. Financial services firms are particularly aligned to this statement of flexibility, with 31% indicating they strongly agreed.

Many are seeking flexibility from suppliers. While 58% of enterprises say they are not seeking flexibility from their IT suppliers, notable segments of respondents say they are asking for or expecting flexibility on payment terms (32%), pricing (25%) and payment models (22%).

There is a great deal of additional detail to be gleaned viewing responses to these questions by different combinations of company size, vertical, state of transformation and other factors. Look for a deeper dive forthcoming from our regular coverage of technology pricing.

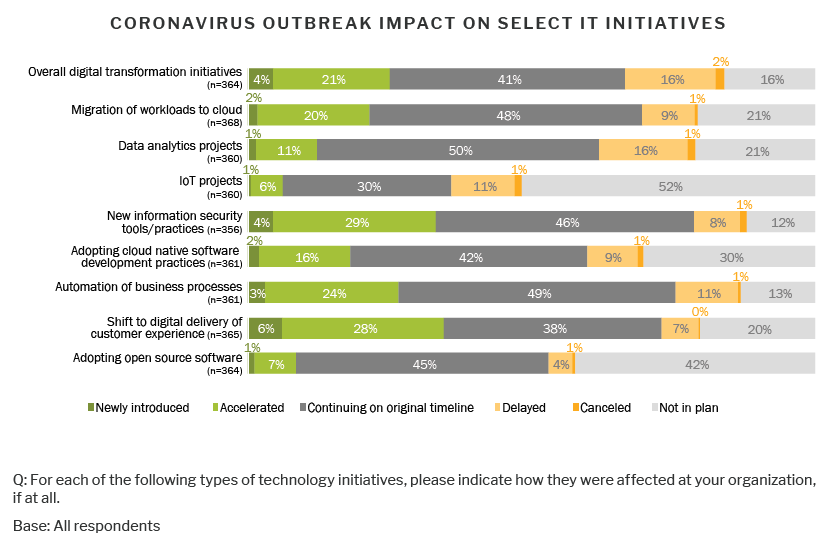

Organizations are reporting both acceleration and slowing of IT initiatives in a variety of areas as an outcome of the coronavirus outbreak. However, these disruptions are the exception, with most plans continuing according to their original timelines.

The outbreak is driving transformation in key areas. Enterprises that report introducing or accelerating IT initiatives outnumber those that are delaying or canceling by a factor of 5:1 in the area of digital delivery of customer experience, by 3:1 for new information security tools and practices, and by roughly 2:1 for cloud migration, process automation and adoption of cloud-native software development practices.

Some specialized initiatives are slowing. IT initiatives for which delays and cancellations outnumber acceleration and introduction include IoT projects (by a factor of 2:1) and data analytics projects (by less than 2:1). While these initiatives are core IT practices for some organizations, as emerging technology practice areas they may be more likely to have been at experimental or proof-ofconcept stages that justified pauses in development.

However, disruption is the exception. For all initiatives tested, the largest portion of respondents say they were continuing according to original timelines.

These IT initiatives are broadly selected, distinct, mapped closely to 451 Research’s coverage channels, and influenced significantly by factors such as company vertical and digital transformation status. Expect to see more detailed coverage of the impact on IT initiatives throughout our channel coverage

Vendors must build to suit the new ways of working. Technology suppliers should already be building and packaging their offerings around the changing requirements of businesses – not only addressing the immediate demands of isolation and remote work, but also acknowledging and supporting the more permanent shifts in ways of working, as exhibited by the 67% of organizations reporting permanently expanded WFH policies, and the 47% planning office footprint reductions.

Create technology solutions to major new operational hurdles. Businesses broadly agree that social distancing will be the biggest operational challenge in returning to work. But it comes accompanied by a range of employee health and safety challenges, customer pipeline issues, transformation requirements and other demands. Businesses will look to technology vendors for new strategies to address these in the immediate future, and these vendors should design their new capabilities accordingly.

Technology vendors must understand the IT priorities that surround their offerings. Enterprises are variously accelerating and pausing IT projects across cloud, analytics, IoT, digital customer experience, overall digital transformation and other areas. Technology vendors and service providers should intimately understand the factors that influence those decisions to support those judgements and potentially influence demand. They may have to encourage organizations not to halt transformation initiatives by specifically illustrating the value within their new circumstances.

Flexibility is a necessity. While not all customers will require flexibility in pricing, payment models or terms, few –if any – markets are immune to the need for flexibility, and many technology vendors have already been working to bring as-a-service-style pricing models to products and services that traditionally had more static pricing. The impact of inflexibility could range from damaged relationships to lost customers.

451 Research runs a panel of highly accredited senior IT executives. Members of this proprietary panel, which consists of IT decision-makers, participate in surveys focused on enterprise IT trends. Respondents of this flash survey are members of the panel who were qualified based on their expertise in their organizations’ IT deployment. Delivered quarterly, this research provides comprehensive, survey-driven analyst reports with customizable data deliverables.

The Voice of the Enterprise: Digital Pulse survey wave was conducted in Q2 2020. The survey represents approximately 575 completed questionnaires and 25 hour-long interviews from pre-qualified IT decision-makers. This survey was designed to measure the impact of the COVID-19 coronavirus outbreak on businesses